June 22, 2022

Dear Investors and Friends,

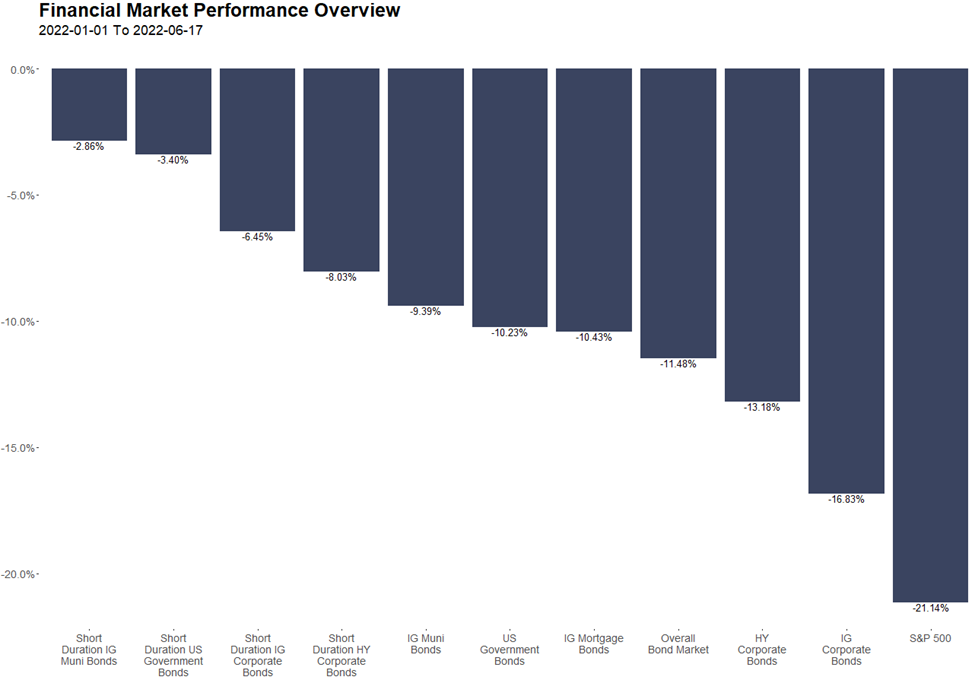

It has been a tough year for investors. No matter where you look, global financial assets have gotten crushed and with heightened inflation rearing its ugly head for the first time in the US in nearly forty years, even cash has offered little solace. What has been unique about this sell-off is that “defensive” asset classes have sold off right along with “offensive” asset classes. As the chart below shows, US Treasury bonds, which historically have enjoyed a negative correlation with stocks during times of turmoil, are down significantly, right along with risk-seeking assets like the S&P 500.

For the last few decades, conventional wisdom held that a 60/40 portfolio – a portfolio comprised of 60% stocks and 40% bonds - would buffer investors against market downturns - as stocks sold off the bonds would appreciate. Because no financial assets have been spared this time - bonds have sold off right along with equities - we are calling this across-the-board reduction in valuations the Great Reset.

What Is Different About This Downturn

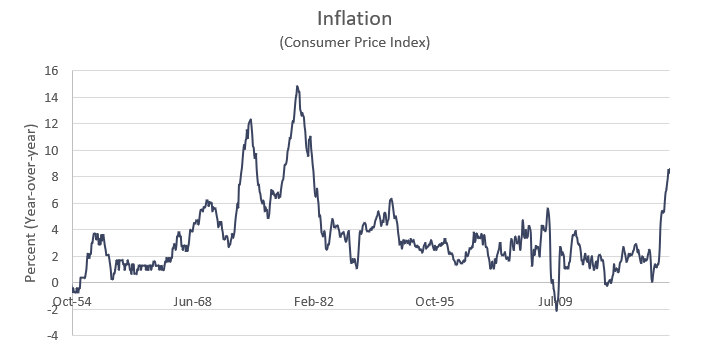

Most market downturns occur because something happens in the economy that threatens growth. In the Great Financial Crisis, the crash of the housing market led to a credit crunch that stifled economic activity. In the Dot.Com bust, rampant speculation in technology stocks, many of which never generated revenue let alone a profit, came crashing down resulting in a recession. Growth, however, is a balancing act. The financial asset price meltdown that we are experiencing now is because of too much growth. The pandemic unleashed an unprecedented level of global fiscal and monetary stimulus that not only blunted the impact of stifled worldwide activity but subsequently overheated large swaths of the international economy. The pandemic also closed off significant portions of the labor force exacerbating supply chain issues just as demand was increasing due to government stimulus. As we all learned in Econ 101, when demand exceeds supply, price goes up. That is called inflation. As the chart below shows inflation has now reached a 40-year high.

How Too Much Growth Leads to Lower Bond Prices

The mechanism by which too much growth wreaks havoc on bond prices is as follows:

The market simply takes expected future cash flows and discounts them based upon prevailing interest rates. Because interest rates used to discount future cash flows have gone up, the discounted future cash flows are lower, hence today’s price is lower.

Contrast the diagram above with the typical downturn we experience.

What Has the Fed Done in Response to Excessive Inflation & What Is Priced In

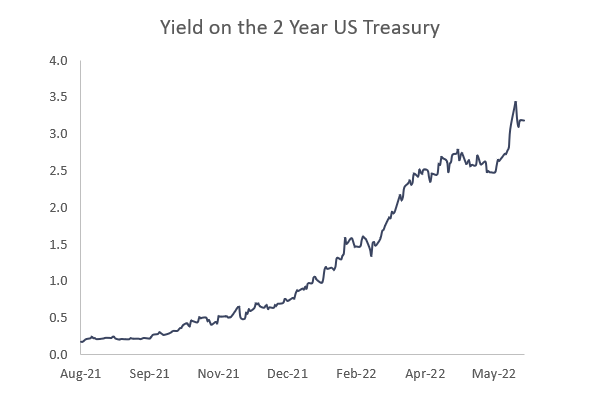

Taking this framework back to the here and now, the US Federal Reserve has hiked the Fed Funds rate 3 times this year – 0.25% in March, 0.50% in May, and we just had the biggest hike since 1994, 0.75%, last week. Higher borrowing costs slow borrowing, reduce economic activity and hence lower inflation. This is just the beginning, additional hikes are priced in. The yield on the two-year US note, the Treasury most sensitive to expected rate hikes, is an excellent indicator of what the market anticipates the Fed doing. As can be seen below, the yield on the 2 Year Treasury has increased from 0.20% in early September of last year to as high as 3.43% last week.

How the Fed Manages Inflation by Managing Our Expectations

In a report delivered to Congress this past week the Fed said, “The Committee’s commitment to restoring price stability … is unconditional“ (emphasis added). Why such strong language? A key variable in future inflation is the expectation today of future inflation. For example, if people expect prices to rise 5% over the next year, businesses will raise prices by at least that much and workers will demand similar-sized raises. So, all else equal, if inflation expectations rise by 5%, actual inflation will tend to rise by 5% as well. Powell is signaling to market participants that he will do whatever is necessary to “re-anchor” inflation expectations to the central bank’s 2% inflation target. Do we believe him? Yes. He now understands that the inflation we are experiencing is neither transitory nor temporary and he is well versed in the lessons of the Volcker era. But taming inflation may come at a cost.

Recession Risk

Inflation is restrained by raising interest rates. Higher interest rates reduce growth. A reduction in growth may lead to a recession. Powell is walking a tight rope. If he raises rates too much and / or too quickly he will cause a recession. Raise rates too little or too slowly you get runaway inflation. Powell has thrown down the gauntlet – he is going to reduce inflation – the question is – can he avoid creating a recession in the process. If he is unable to do so, expect a “normal” downturn and higher bond prices pursuant to the process already discussed:

What Does This Mean for RCM Investors

As high yield bond investors we face two major risks – default risk and interest rate risk.

We manage default risk by being laser focused on the underlying fundamentals of each issuer / bond we invest in. In a time such as this where the risk of a recession is elevated, we are particularly focused on credits that have the resources to meet near term debt obligations. Year to date, however, we have sold no positions out of default concerns.

We manage the risk that interest rates will continue to rise by investing in shorter duration bonds. Does that mean we will be unscathed, at least on a mark-to-market basis, in a rising interest rate environment– no. Short term, returns are largely a function of price movements – something we have no control over. Fortunately, though, long-term returns, barring a default, are 100% a function of the yield at which we deploy capital and the volatility of the market - the higher the yield and the higher the volatility, the higher the return. That means that this environment, while temporarily painful, should allow us to generate higher returns for investors over the medium to long term, all else equal.

Please reach out to us with questions and comments. Thank you for trusting RCM with your capital. It is a privilege for us to serve you.

David and Mike

Disclaimer

Roosevelt Capital Management LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Past performance is not indicative of future performance. Principal value and investment return will fluctuate. No guarantees or assurances that the target returns will be achieved, or objectives will be met are implied. Future returns may differ significantly from past returns due to many different factors. Investments involve risk and the possibility of loss of principal.

The performance and characteristics information contained herein is for accounts solely managed by David Roosevelt, Managing Member of Roosevelt Capital Management LLC. Investment performance and characteristics through September 2019 are for Roosevelt Investments accounts managed by David Roosevelt. Investment performance and characteristics for October 2019 and thereafter are for Roosevelt Capital Management accounts managed by David Roosevelt. The performance information has been certified by ACA Compliance through December 31, 2018 and is available upon request. The values and performance information contained herein do not reflect management fees. While all the values used in this report were obtained from sources believed to be reliable, all calculations that underly numbers shown in this report believed to be accurate, and all assumptions made in this report believed to be reasonable, Roosevelt Capital Management LLC neither represents nor warrants the reports, values, calculations or assumptions and encourages each prospective investor to conduct their own review of the reports, values, calculations and assumptions.