April 25, 2023

Dear Investors and Friends,

The increase in interest rates that began in 2022 sent shockwaves through every corner of the market and woke investors up to three stark realities:

- Higher inflation is back after a nearly 40-year hibernation,

- Interest rate risk is real as evidenced by the destruction in value of longer duration “risk free” assets, and

- For the first time in well over a decade, there is significant opportunity cost to holding cash.

Below we discuss how RCM’s strategies have performed in this time of significant volatility and uncertainty.

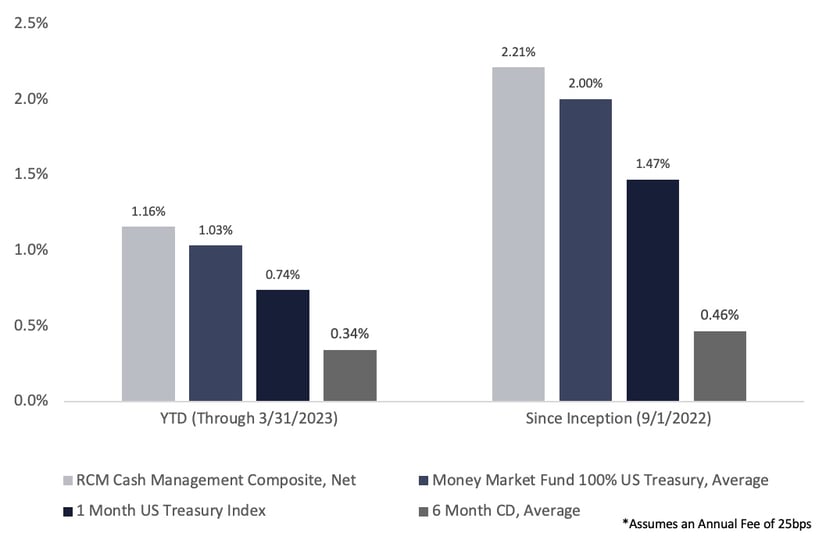

Performance of RCM’s Cash Management Composite

RCM’s cash management strategy endeavors to maximize investor returns while taking no default risk (we only invest in US Treasuries), limited interest rate risk (in this environment we only go out the curve 6 months), minimal counterparty risk, and exceptional liquidity, with the added benefits of being turnkey and customized to specific client constraints. To date the strategy has surpassed its objectives.

RCM Performance: Net Returns Through 03/31/2023, Not Annualized*

Two major observations can be made about the above:

- First, through active management and after fees, RCM was able to generate returns meaningfully higher than money market funds and 1 Month Treasuries, and

- Second, holding money in a bank, as represented by the 6 Month CD, is a significant drag on returns in this environment, not to mention exposes the investor to counterparty risk.

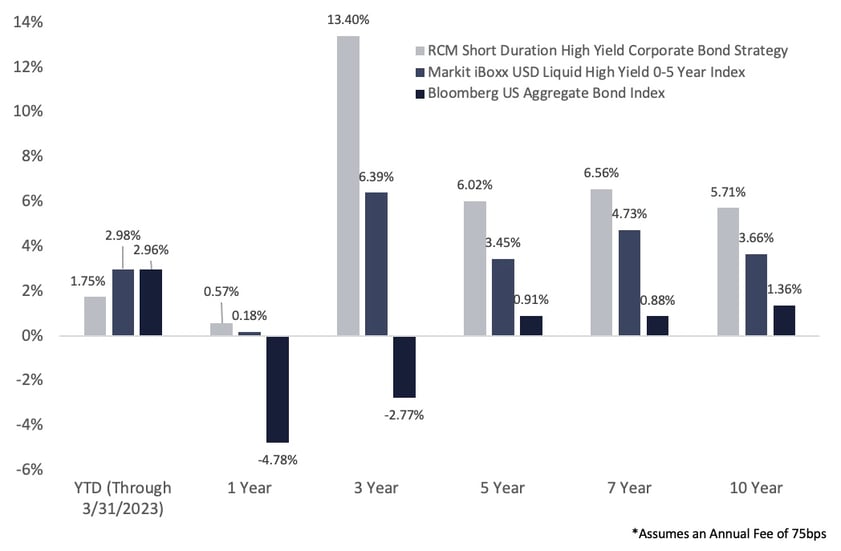

Performance of RCM’s Short Duration High Yield Corporate Bond Composite

While we never like reporting that our short duration high yield composite is not beating its benchmarks, in the short run there will be periods in which underperformance is inevitable, and the first quarter was one of those. Over the medium to long run, RCM has significantly outperformed its benchmarks.

RCM Performance: Net Returns Through 03/31/2023, Annualized Except YTD*

A couple observations about the above:

- First, despite significant market volatility during Q1 because of Silicon Valley Bank and fear over additional bank runs, bonds performed well, and

- Second, the Bloomberg US Aggregate, which most people consider representing the “bond market” like the S&P 500 represents the “stock market,” has been a perennial laggard vs. short duration high yield over longer periods.

Near Term Market Drivers

Earnings and the debt ceiling debate will be the likely near-term market drivers. Earnings season has begun and so far, performance has been robust, reducing the probability of an impending recession but increasing the probability of higher rates for longer. The US debt ceiling debt debate is coming into sharper focus as upcoming tax receipts will shed increased light on the Treasury’s ability to service its debt. We will learn more about both over the next few weeks.

We do not know what the future holds, but our processes for asset allocation, security selection and portfolio optimization provide us great conviction that in our cash management strategy we will continue to outperform over the short, medium, and longer terms, and in our short duration high yield strategy over the medium and longer terms.

Please reach out to us with questions and comments. Thank you for trusting RCM with your capital. It is a privilege for us to serve you.

Dave and Mike

Disclaimer

Roosevelt Capital Management LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Past performance is not indicative of future performance. Principal value and investment return will fluctuate. No guarantees or assurances that the target returns will be achieved, or objectives will be met are implied. Future returns may differ significantly from past returns due to many different factors. Investments involve risk and the possibility of loss of principal.

While all the values used in this report were obtained from sources believed to be reliable, all calculations that underly numbers shown in this report believed to be accurate, and all assumptions made in this report believed to be reasonable, Roosevelt Capital Management LLC neither represents nor warrants the values, calculations or assumptions and encourages each prospective investor to conduct their own review of the audits, values, calculations and assumptions.